Marios Stamatoudis’ Trading Strategy

Marios Stamatoudis will tell you, with a disarming lack of vanity, that he is not the fastest man in the room.

He is not the most precise, not the most accurate, not especially quick to adjust. “I’m not that smart of a guy,” he says — the kind of self-assessment that, from most people, would be false modesty, but from Stamatoudis lands as something rarer: the product of genuine forensic self-examination. He is, instead, the kind of person who finds a thread and pulls it until the whole thing unravels. He goes deep. It is, as it turns out, exactly the right quality for the career he has built.

His Background

He came to trading the way most young men come to it: through a social media ad. He was eighteen, drawn to the flash and speed of day trading — the adrenaline, the action, the promise that the screen could make you rich before lunch.

For the first four years, he was a day trader. He made money. He found his initial profitability there. But he also found something else: a gnawing misalignment between what the craft demanded and who he actually was. Day trading requires precision, fast reflexes, and the ability to absorb serial losses without flinching. Stamatoudis, by his own accounting, was none of those things.

He was slow, he made mistakes under pressure, and every drawdown — every single one — registered as real money, because day traders close positions nightly and reset to cash. There was no portfolio cushion, no time for the trade to breathe. Every loss was personal.

The catalyst for change came in 2020, during one of the most extraordinary market environments in recent memory. He watched stocks he had entered as day trades — tight entries, good timing — simply explode.

Not 10, not 20, but 200 and 300 percent. Moves that would have rewarded someone who simply bought and waited. “If I just went on that stock, bought, put my stop break even, and went on vacation for a month,” he recalls, “I would have made more money than battling with the tape each and every single day.” It was not an epiphany so much as a permission slip. He could stop fighting himself.

He took time off. He read. He found the momentum trading literature — O’Neil, Minervini — and recognized in it the architecture of a system that might actually suit him.

The transition took years and nearly cost him the game entirely; around his third year in markets, he came close to quitting. What kept him was not discipline in the motivational-poster sense, but something more specific: love of the problem, and the support of a partner who understood what the profession actually costs.

Marios‘ Trading Philosophy

At the center of Stamatoudis’s worldview is a single, organizing conviction: the market is asymmetric, and almost no one is exploiting that asymmetry aggressively enough.

He is skeptical of dogma — “I hate dogma in trading,” he says more than once — and distrustful of the copy-paste culture that dominates retail trading education. He believes the holy grail most traders are searching for does not exist, and that the search itself is the error. The real work, in his view, is not finding the perfect setup but building a system that is structurally aligned with one’s own temperament and cognitive strengths. “You need to find the style that really elevates the strength of you,” he says, “and hedges against your weaknesses.”

His relationship with loss is worth examining carefully, because it is counterintuitive. Stamatoudis accepts — and has mathematically embraced — a win rate that would unnerve most traders. He trades with roughly a 20 to 25 percent success rate. That means, in any given month, based on his trading frequency, he can expect 14 to 15 consecutive losing trades. Not occasionally. Every single month.

His system is built to absorb that reality. What it relies on, structurally, is the outsized return of the trades that do work — the outliers — to more than compensate. “One outlier can make me back 50, 60, 80 times,” he says. His system is not a war of attrition; it is a patient waiting game for low-frequency, high-magnitude events.

This acceptance of serial losses without abandoning the system is only possible, Stamatoudis argues, if a trader understands what he calls the “normalities” of their approach — the statistical baseline of what a system actually produces, not what one hopes it produces. Surprise, he argues, is the root of most trading psychology failures. “It’s the element of surprise that creates the problems.” When you know that 15 consecutive losers is not a disaster but a predicted feature of your system, you do not panic. You simply wait.

The Trading Strategy That Produces The Big Wins For Marios Stamatoudis

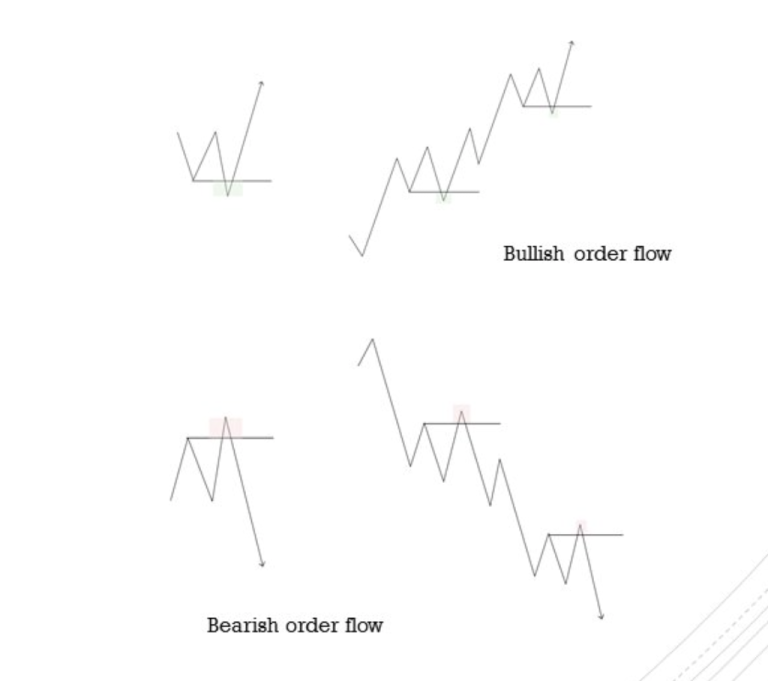

Stamatoudis is a momentum swing trader, hunting for what he calls outlier trades: breakout setups in individual stocks with the compositional qualities — technical, fundamental, thematic, and narrative — that have historically preceded massive multi-week or multi-month moves.

The technical foundation is built around extremely tight stops, a feature he arrived at not by intuition but through rigorous back-testing. He discovered something he describes as a “mathematical ledge” in the relationship between stop width and win rate: the relationship is not linear.

Cutting stop width in half does not halve win rate. It might reduce it by a third. The result is that expectancy — the product of win rate and reward-to-risk — improves dramatically through compression alone. “Synthetically, you created an edge from a brute force adjustment without doing anything,” he says. He uses stops as tight as 0.5 ATR, a width institutions cannot operationally replicate, which is precisely the point. The edge exists partly because it is inaccessible to large capital.

Tight stops also enable large position sizing. Because his risk per trade is small in percentage terms (roughly 0.2 to 0.3 percent of capital), he can take meaningful positions at entry — rather than scaling in — and move his stop to breakeven quickly once a trade moves in his favor. A risk-free position, in his framework, becomes a ticket to hold through volatility and wait for the outlier.

Beyond the technical, he has built a research process for identifying what he calls the “DNA” of outlier stocks — the compositional fingerprint that historical winners share.

This involves studying decades of big movers, identifying commonalities in price structure, volume, fundamentals, narrative, and thematic alignment, and translating those into filters that tighten his tracking universe. He currently monitors roughly 300 names, from which he makes 400 to 500 trades per year. Of those, roughly 10 to 15 will be true outliers, responsible for approximately 80 percent of his annual gains.

Themes are an essential layer of this process. Stamatoudis tracks stocks by keyword clusters — grouping names by their operational exposure to emerging economic or technological phenomena — and monitors when price structures in a cluster begin to accelerate simultaneously.

He offers quantum computing stocks in late 2024 as a recent example: a single leader (IONQ) showed footprints he recognized, and within weeks a cluster of similar names exhibited the same structures. The theme confirmed itself through repetition. He was already positioned.

He uses AI, increasingly, to handle the parts of this research that are behavioral and narrative in nature: analyzing the quality and novelty of company news, assessing thematic purity, parsing sentiment signals from public discourse. He is careful about the limitations — AI, he notes, is unreliable in mathematics and price action analysis — but for the behavioral and qualitative dimensions of stock selection, he finds it genuinely useful. He envisions what he calls the “hybrid trader”: a discretionary mind augmented by AI’s capacity to process narrative and sentiment at scale. It is, he believes, the next edge.

not making money?

U.S. Investing Champion

The numbers Stamatoudis shares are specific enough to be meaningful. In the U.S. Investing Championship — a real-money competition with independently verified results — he posted a return exceeding 290 percent.

Within that performance, approximately 10 outlier trades were responsible for 80 percent of the gains. His average risk per trade is 0.2 to 0.3 percent of capital; a 30R outlier — a trade that returns 30 times his risk — produces roughly 8 to 9 percent in a single position. He runs fixed risk, not dynamic, because his back-testing showed it produces smoother drawdown profiles than dynamic sizing applied over a system with his win rate distribution.

What makes the edge durable, in his telling, is that its foundations are structural and behavioral rather than arbitraged. Breakouts have occurred for hundreds of years. Climax tops have occurred for hundreds of years. The human psychology that produces them has not changed.

“Math never lies and never changes,” he says. The specific calibrations — where exactly to set a partial, how quickly to move to breakeven — will drift and require adjustment. But the core principle, that outliers exist, that tight stops create asymmetric expectancy, that themes amplify individual moves, will not.

Whether Stamatoudis becomes what he intends to become — the first world-class hybrid trader, — remains, of course, an open question. He is nine years into a game that has a way of humbling even its most rigorous students.

But the intellectual architecture he has built is coherent, empirically grounded, and deeply personal in the best sense: it was not copied. It was constructed, piece by piece, from the raw material of who he actually is. That, he would say, is the only kind of edge worth having.

Kraeen Jeffs– Stocks & Futures Trading . You can read profiles on other great traders like Steven Dux, Alex temiz, Brando, Modern Rock & many more

not making money?

{kind=link}